What are the three stages of government accounting?

Olivia Hensley

Olivia Hensley

Then, what are the 3 steps of accounting?

There are three steps in the accounting process those are Identification, Recording and Communicating.

Also, what is government accounting process? Government accounting is the process of recording, analyzing, classifying, summarizing communicating and interpreting financial information about government in aggregate and in detail reflecting transactions and other economic events involving the receipt, spending, transfer, usability and disposition of assets and

Also Know, what are the stages of accounting system?

The eight steps to the accounting cycle include the following:

- Step 1: Identify Transactions.

- Step 2: Record Transactions in a Journal.

- Step 3: Posting.

- Step 4: Unadjusted Trial Balance.

- Step 5: Worksheet.

- Step 6: Adjusting Journal Entries.

- Step 7: Financial Statements.

- Step 8: Closing the Books.

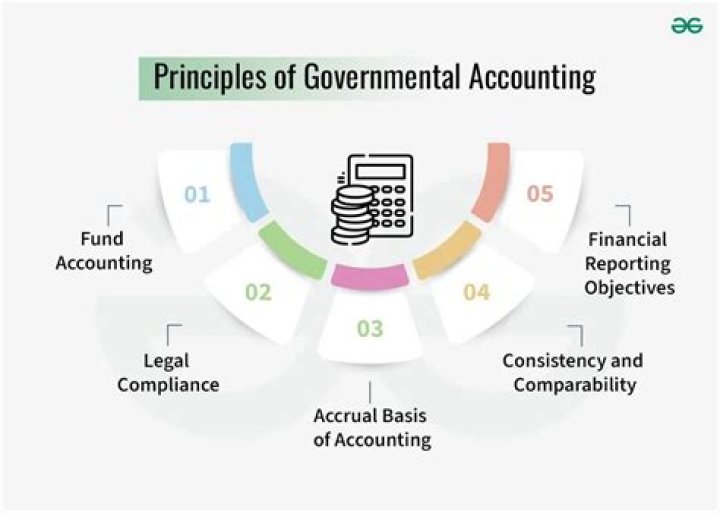

What are the 13 basic governmental accounting principles?

Terms in this set (15)

- accounting and reporting capabilities.

- Fund accounting systems.

- types of funds.

- number of funds.

- reporting capital assets.

- Valuation of Capital Assets.

- Depreciation of Capital Assets.

- Reporting Long-Term Liabilities.

Related Question Answers

What is basic accounting skills?

An accountant should know how to prepare financial statements and accounting reports for planning, controlling, budgeting and decision-making. The three key financial statements are balance sheet, profit & loss and cash flows account. These above three financial statements are interlinked with each other.What is the first step of accounting?

The first four steps in the accounting cycle are (1) identify and analyze transactions, (2) record transactions to a journal, (3) post journal information to a ledger, and (4) prepare an unadjusted trial balance.What is the last stage of accounting?

In the accounting cycle, the last step is to prepare a post-closing trial balance. It is prepared to test the equality of debits and credits after closing entries are made. Since temporary accounts are already closed at this point, the post-closing trial balance contains real accounts only.What are the 5 basic principles of accounting?

What are the 5 basic principles of accounting?- Revenue Recognition Principle. When you are recording information about your business, you need to consider the revenue recognition principle.

- Cost Principle.

- Matching Principle.

- Full Disclosure Principle.

- Objectivity Principle.

What is recording process in accounting?

Every accounting process of a transaction starts with identifying and analyzing. Under this process, all the important transactions that pertain to a business entity are recorded. After the identification and analyzing process, the transaction goes through the process o recording it in a journal.What is the full accounting cycle?

Full cycle accounting refers to the complete set of activities undertaken by an accounting department to produce financial statements for a reporting period. Full cycle accounting can also refer to the complete set of transactions associated with a specific business activity.What is the process of recording transactions in a journal is called?

A journal may be defined as the book of original or prime entry containing a chronological record of the transactions from which posting is done to the ledger. The process of recording the transactions in a journal is called as journalizing.What is the 10 Step accounting cycle?

10 Steps of the Accounting CycleTransferring journal entries to the general ledger. Crafting unadjusted trial balance. Adjusting entries in the trial balance. Preparing an adjusted trial balance.

What is the ideal time period of accounting?

The accounting period usually coincides with the business' fiscal year. However, there are many business entities that follow the accounting period of three months or six months. Internally, the accounting period is considered to be a month or a quarter while externally it is for a period of twelve months.What is difference between bookkeeping and accounting?

Bookkeeping is all about recording and organising financial data while accountants take that data to prepare reports and get them ready for HMRC.Which is the most important step in the accounting process?

The fundamental concepts above will enable you to construct an income statement, balance sheet, and cash flow statement, which are the most important steps in the accounting cycle.Which stage of reimbursement accounting is the final stage?

The final stage of reimbursement accounting. A voucher from DFAS is received to start the billing event for this customer in reimbursement accounting.What is the objective of accounting?

In a practical sense, the main objective of financial accounting is to accurately prepare an organization's financial accounts for a specific period, otherwise known as financial statements. The three primary financial statements are the income statement, the balance sheet and the statement of cash flows.What are the 7 steps of accounting cycle?

We will examine the steps involved in the accounting cycle, which are: (1) identifying transactions, (2) recording transactions, (3) posting journal entries to the general ledger, (4) creating an unadjusted trial balance, (5) preparing adjusting entries, (6) creating an adjusted trial balance, (7) preparing financialWhat are the limitation of accounting?

One of the biggest limitations of accounting is that it cannot measure things/events that do not have a monetary value. If a certain factor, no matter how important, cannot be expressed in money it finds no place in accounting.What is the most important output of the accounting cycle?

The process that begins with analyzing and journalizing transactions, and ends with the post closing trial balance is called an accounting cycle. The most important output of the accounting cycle are the financial statements.What is core accounting process?

The accounting process is three separate types of transactions used to record business transactions in the accounting records. This information is then aggregated into financial statements. The third group is the period-end processing required to close the books and produce financial statements.How is government accounting different?

"Unlike the financial (for-profit business) accounting, in the governmental accounting, the consumptions are not calculated as part of the facility assets. The accounts of the governmental accounting do not discriminate between the capital expenses and the current revenue expenditures."Why is government accounting important?

Recording and monitoring the studies and activities of the governments regarding financial and economic policies, government accounting is the most important element of the principle of financial transparency and financial accountability in this regard.What is accounting rules and regulations?

Generally accepted accounting principles, or GAAP, are a set of rules that encompass the details, complexities, and legalities of business and corporate accounting. The Financial Accounting Standards Board (FASB) uses GAAP as the foundation for its comprehensive set of approved accounting methods and practices.Is Government Accounting Public or private?

Private accounting is concerned with the inner workings of businesses, governments and agencies. Private accountants work for specific companies and are an important part to the success of any organization. For this reason, many public accountants eventually work in the private sector.What are the limitations of government accounting?

The following are the main limitations of the new accounting system: It is mostly based on the cash system. No record is made relating to accrual transactions and hence, it cannot show the real financial situation of the government.What is the difference between GAAP and GASB?

So, "the Government Accounting Standards Board (GASB) was created in 1984 to establish generally accepted accounting principles (GAAP) for state and local government entities," says Reference for business. GASB cannot be and is not part of GAAP. But, GASB does follow GAAP standards.What is the accounting equation for governmental fund?

In governmental accounting the resources of the government are accounted for in "funds". "Funds" are defined as an independent accounting entity with a self-balancing set of accounts. In other words, within each fund, the basic accounting equation (Assets = Liabilities + Equity) still applies.What are the basic fund types used by government?

GOVERNMENTAL FUNDSFour fund types are used to account for a government's “governmental- type” activities. These are the general fund, special revenue funds, debt service funds, and capital projects funds.

What does GASB stand for in accounting?

Governmental Accounting Standards BoardWhat are the characteristics of government accounting?

Features Of Government Accounting- Profit And Loss. Since government is a public institution, its main objective is to maintain law and order in the country.

- Government Regulations. Government accounting is maintained according to government rules and regulations.

- Double Entry System.

- Budget Heads.

- Budgetary Control.

- Banking Transaction.

- Auditing.